Let’s face it – we aren’t very good at saving. The average savings rate for individuals from year-to-year fluctuates in the single digits as a percentage of what we earn. There is a lot of truth to the saying “We live as if there’s no tomorrow” Well guess what? Tomorrow is here and we unfortunately still fail to see it. The longer we put off saving for tomorrow will only result in a reduced standard of living tomorrow. The fintech community is stepping up to meet this challenge. Here you will find the latest tools, tips, and technology designed to help you save for you tomorrow. For example, see 5 lazy ways to make saving easy.

Moving out of the house for the first time is one of the biggest steps you will ever take in your life. Yes, it’s thrilling. Yes, it’s scary. And that’s what makes it such a perfect introduction to life on your own.

Living independently will take some getting used to, particularly when it comes to finances, but you can ease the transition with some strategic preparations. When it’s time to venture out on your own, these five tips can help you get a solid start:

Move when you’re ready

First of all, if you’re not ready to move out, don’t. The fact that you have reached a certain age is not reason enough to fly the coop. Ensure you’re prepared for the realities of living independently. Think about your financial stability, and factor in the costs of your new home and lifestyle away from your parents. Honestly assess your situation, and take time to save money if necessary.

Start budgeting

It’s really never too early to learn how to budget, but you definitely need to understand the basics before moving out. Draw up an estimate of all your monthly expenses, and compare it to your income. Then, determine which expenses are fixed, distinguish between your needs and wants, and snip what you must. If you haven’t found a home yet, Interest.com recommends allocating about 28% of your income for rent.

Drop the cable

Thanks to various streaming services one expense that’s easy to cut is the cable. There is all the entertainment you could ask for, and they cost a fraction of what a cable subscription costs. However, costs can quickly add up if you pile up à la carte channels that you never use. Only subscribe to the channels and features you need, and compare devices and apps to find your best option.

Automate your finances

Another great way to save money is to automate your finances. In short, automation simplifies the process of saving and allocating your money where you want it to go. Make sure you have a primary checking account and keep at least 25% of one month’s expenses in it at all times. Then, set your account up to automatically put a portion of each paycheck into your savings account. From there, you can set up automatic electronic payments for as many bills as possible.

Furthermore, you can even set automatic deposits for your retirement savings and investment accounts. Automation not only makes it easier to know where your money is going, but it can also save you from missing important payments and harming your credit score.

Develop good habits

Finally, if you haven’t already, you will want to start forming habits that are conducive to your independent lifestyle. Come up with a decluttering routine that helps you keep a comfortable living space each day, and do laundry at least once a week. Figure out what groceries you need for a healthy diet, work them into your budget, and look into meal planning. Also, make sure you’re going to bed at a decent time because your whole life is better if you’re well-rested and energized.

Proper preparations for your big move will make it an experience to cherish for the rest of your life. Remember to assess your situation to make sure you’re ready to go out on your own, and learn the fundamentals of budgeting. Figure out what expenses you can cut (like cable), and automate your finances to make saving and allocating your money easier. And start developing good habits that will help you succeed in an independent life. Most of all, take a deep breath and embrace the adventures that lie ahead!

The article above was a guest article by Brittany Fisher from Financially Well

As interest rates have continued to climb from historically low levels it is important that you optimize your money. This is especially true for cash accounts such as checking and savings. The best way to do this is to check with your bank and or brokerage to see if your “Core” account is a simple FDIC insured account which only yields a very small percentage or if it is in a money market account which is currently yielding just over 2%. This might not seem like much but can really add up for anyone currently holding a large cash position in anticipation of a significant upcoming purchase like a home.

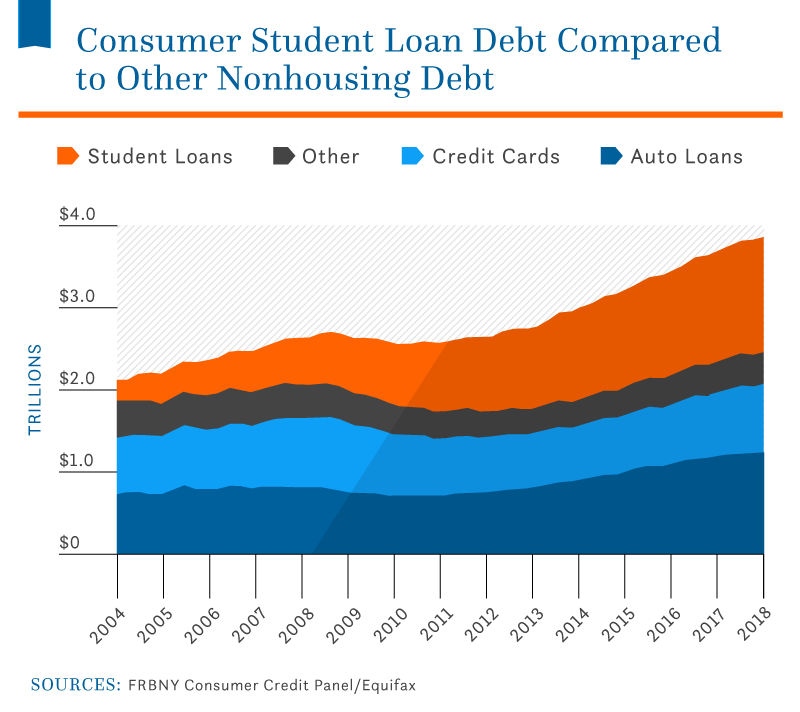

College tuition prices are rising exponentially each year and 44.7 million* Americans have student loan debt. The average monthly student loan payment is $393*. Student loan debt is by far the largest burden for most Americans today. With this in mind, saving for your child’s college education is one of the most important things you can do for their future. U-Nest is working to change this but before we talk about what U-Nest and what it can do for you let's take a look at some of the current college debt statistics as well as some of the ways you can save for college.

In order to maximize the money put away for your child’s education, there are a few options that are more beneficial than a standard savings account. The most common of these is a 529 plan, but UGMA/UTMA custodial accounts or a Coverdell ESA are also available. Keep in mind that these accounts were developed as a tax benefit for you to use as a tool in order to help incentivize you to save more for this growing burden.

529 Plan

A 529 plan is an investment account offering both tax-free earnings and withdrawals, given the money is used to pay for qualified educational expenses. Typically any expense involved in the enrollment of a student to a post-secondary education institution qualifies, such as tuition, room and board, and even computers. With a 529 account, you are able to change the beneficiary to another child or to yourself and the money never expires. The three primary advantages of a 529 are: the account grows tax-free, the parents retain control of the account, and there is minimal impact on financial aid award packages.

UGMA and UTMA Custodial Accounts

UGMA (Uniform Gift to Minors Act) and UTMA (Uniform Transfer to Minors Act) are custodial accounts used to hold and protect assets for minors until they reach a certain age in adulthood. Depending on the state, this could be when they turn 18. The account is considered the property of the minor, therefore a portion of the investment income is untaxed, while an equal portion is taxed at the child’s rate rather than the parents’. Money can be withdrawn without penalty for any expenses that benefit the child, not just educational ones. You can read more about the differences between a UGMA and UTMA account.

Coverdell ESA’s

Coverdell ESA’s (Education Savings Accounts) are similar to 529 plans in that they offer tax-free earnings and withdrawals given the money is spent on qualified educational expenses. Differing from a 529 plan, Coverdell ESA’s allow funds to be used for certain K-12 educational expenses. They are only available for families below a certain income level and have a much lower maximum contribution limit than a 529 plan. If you would like to learn about additional guidelines surrounding Coverdell accounts HERE is a good guideline and description.

The U-Nest 529

As you can tell from the options above – a 529 not only has the most flexibility it is also the most common when it comes to saving for college.

One of the best ways to open a 529 plan is with U-Nest. U-Nest is an app for iPhone and Android that makes opening a 529 plan easier than ever before. In just five minutes, you can open a 529 plan that has been selected from hundreds of financial institutions and State providers by financial experts at U-Nest. Within the app, you can set up monthly contributions and easily check the account balance at any time.

We interviewed the founder, Ksenia Yudina, who is a Chartered Financial Analyst and entrepreneur with over ten years of experience in the financial industry. In the interview, Ksenia stated that 70% of people don’t know a 529 exists, and only 14% of people are actually using one. U-Nest aims to solve this problem by making optimized 529 plans easily accessible to anyone, regardless of financial status.

U-Nest acts as a digital financial advisor and rebalances accounts over time to achieve a more conservative asset allocation as children get older. Unlike financial advisors that can cost upwards of $200 per hour, U-Nest has waived all underlying broker-dealer commissions, and the advisory fee is a simple and transparent $3 month. In addition, the minimum investment to open an account is just $25.

Visit the U-Next website to learn more about how you can get started.

The Top Tools, Tips, and Technology To Save Money in 2019

This post may contain affiliate links. Please read my disclosure for more info.

One of the first steps of securing your future is to save money. When you save money you can get out of debt faster, invest for your future, gain the flexibility and options to do what you want and perhaps one day have enough saved to be able to retire. Instead of burying your head in the sand, first, recognize that you aren’t alone and you might be surprised at where you stack up among your peers when it comes to saving money and net worth. Once you realize you aren’t alone – the path to financial independence becomes much clearer.

One of the fastest ways to reach financial independence is by saving as much as you can of what you earn as possible. By setting aggressive savings goals you'll then have the funds to invest more and begin experiencing the 8th wonder of the World Compound Interest!

Never before has it been as easy to save money thanks to the growth of financial technology in the last few years. The trouble of course is knowing where and how to find money saving opportunities. This guide should help to solve that!

Please note: this article will be updated as new products come online. I have purposely left off the list items that I felt were not worth the time, money, or hassle. After all, time is money!

Saving money can come in many forms. Below you will find how you can…

Save Money Getting Free Stuff

Audiobooks, movies, music, and ebooks.

Your local public library is a free resource that can easily be forgotten…this is especially true since we all have smartphones in our pocket. However, our smartphones require apps and subscriptions in order to listen to an audiobook, movie, music or read an ebook. Now you can combine the power of your smartphone, tablet, or computer into the power of a free resource with the Hoopla Digital app! This app only requires that you have a library card in order to access its content for free. Another app with similar offerings is Overdrive.

WalMart has a website that will send you free samples periodically throughout the year. All you need to do is pay $5 for shipping.

Another great article which lists a number of ways to get paid to test and keep free products comes from the website BirdsOfAFire.

Membership Sites To Save Money

AARP – Did you know that you are able to become a member of AARP at any age? Okay, stick with me here! As a 35-year-old, I was able to join AARP for just $12 for the year. I was also able to sign up CafeCareerCoach for the same $12 at the same time! Believe me…she was thrilled! : ) I discovered an article last year which described the two types of AARP memberships. One “regular” $16 annual membership for those over the age of 50. And an associate membership for everyone else for $12. So what’s the difference between the two memberships when it comes to money saving perks like travel, restaurants, and so much more? Nothing! They are the same! The only exception is that for those under the age of 50 you save $4 on the annual membership. Now you can’t say that AARP doesn’t look out for young people! To sign up visit THIS link.

Recurring monthly and annual bills have become something we all just live with and expect. It’s easy to get lulled into just paying the same or more each and every month for the same service. The reason for this is because you might not be aware that other – cheaper options – exist or that you just don’t have the time to hassle or negotiate with current providers.

Thanks to the internet and a number of new financial technology companies you no longer have these two excuses.

Save Money On Internet, Television and Cell Phone

The website Whistleout allows you to directly compare rates across all internet, television and cell phone service providers. Think of it like the Kayak, or Expedia for travel but with Whistleout you can view saving options across these vital services we rely on every day. When it comes to saving money one of the first places most of us naturally want to look toward is on these monthly recurring bills which always seem to creep up and get more expensive each and every year.

Save Money on Cell Phone Bill

Isn’t it frustrating that each and every month you pay the same amount for your cell phone bill even though some months you use fewer minutes and data than previous months? With Ting, you only pay for what you use. Another similar service to check out is FreedomPop.

Negotiate Your Bills & Subscriptions On Your Behalf

Billfixers is a free service which only keeps 50% of what they save you for the first year. They have a nice interface and all you need to do is create an account and upload a copy of your latest bill you would like them to negotiate for you on your behalf.

Truebill is a service that notifies you of ongoing subscriptions that you might have forgotten about. It does this by connecting to your bank and credit card. Truebill shows your recurring bills, recent transactions, as well as ways to save. Truebill is currently offering a $4.99 per month premium option. The best feature of the premium option automatically takes care of canceling unwanted subscriptions on your behalf. Saving money has never been this easy!

Trim is another service that helps you save on bills and recurring charges. After you create your account on Trim you can securely log in to common subscriptions (Think Comcast, AT&T) where Trim automatically begins working on your behalf by taking advantage of “discretionary credits, discounts, and promotional offers without modifying your plan or service level.” If Trim is able to reduce your bill they charge 25% of what you save on an annualized basis. Trim just recently incorporated a budgeting tool and has a peer comparison tool that is currently in beta that will show the spending habits of people similar to you.

Billshark is a similar service to Trim. They negotiate Internet, Wireless, CableTV and Home Security Bills on your behalf. After you create an account you upload a copy of your bill and they do the rest for you. When it comes to saving money let the sharks take care if it for you!

Clarity Money goes beyond simply watching your subscriptions. They write on their site “we believe in transparency and the power of technology to improve people’s lives. We built a system that analyzes your specific financial situation and works to improve it.” Just recently Clarity was acquired by Goldman Sachs.

Save Up For Anything You Want

iSow: One of the best lessons you can teach a child or teen is how to work and save for something that they want. The website iSow calls itself the “future of gift-giving” With iSow you create a profile which where you can list goals or items that you are saving toward. This profile can then be shared with those that can help you toward your goal.

Qapital is an automated savings app which lets you set up savings goals. When you set up a goal you have the option to:

Do Something

Go Somewhere

Get Something

Pay Off Debts

Just Start Saving

Once you make a selection it asks you how do you want to save. The first option is using the Round-Up Rule which rounds up to the $1.00 when you swipe your card. You can also:

Set & Forget Rule: Set daily, weekly or monthly deposits to make savings automatic.

Payday Rule: Pay yourself first. Save a percentage each time you get paid.

Guilty Pleasure Rule: Put a little in savings whenever you buy the stuff you’re trying to resist.

Spend Less Rule: Set a budget. Come in under. Save the difference.

Freelancer Rule: Set aside 30% for Tax Day every time you get paid.

52 Week Rule: Save $1 week 1, $2 week 2 and so on for 52 weeks.

Apple Health Rule: Reward yourself for hitting fitness goals with Apple Health.

Rumor has it that later this year Qapital will be launching “Qapital Invest” to help users save for mid-term goals, such as a vacation or vehicle purchase. Qapital takes saving for the things you want and the goals you have to the next level. If you want to give it a try sign up here.

Save Money With Cash Back

There are a number of cash back opportunities that exist today. Here I will highlight a couple of my favorites.

SiftWallet gets you automatic refunds when prices drop. You link it to your credit card and it automatically monitors your purchases and gets you a refund if the price drops. I previously purchased some Calvin Klein Boxer Briefs. Soon after, I received a notice from SiftWallet that the price had dropped by $7.48. Soon after, I received a check in the mail for the difference. It was that simple!

Dosh Is a cash-back app that pays you for making purchases once you connect a debit or credit card.

iBotta is an app that gives you cash back on items that you have to buy in a store anyway. When you buy simply scan the barcode of the product and then send a photo of your receipt.

EBates is a well-established cash back program. I use the Ebates Chrome extension on a daily basis. When you are online the extension automatically detects websites where you can earn cash back and how much cash back you are able to earn. All you need to do is click on the button to activate the cash back.

HoneyApp The HoneyApp is an amazing app that allows you to instantly check for every promo code currently available whenever you shop online. The HoneyApp Chrome extension (also available as an extension on all other major browsers) instantly checks for any and all available promo and discount codes available. So now when you see the discount or promo box on that final screen just before you checkout. No longer do you have to leave that box blank or go back to Google to search for promo and discount codes for that particular retailer. Instead, Honey does that work for you by filling in the best any code available from anywhere online for that particular site. Also, since I suspect most of your online purchases are done online on Amazon the HoneyApp works on Amazon no problem! The HoneyApp was started when this guy was just trying to order a pizza online. Thank you, Ryan!

Note: In the past, I have noticed that EBates and HoneyApp don’t play nice with one another so it might be worth testing out both when you go to make a purchase to compare which one can get you the better deal!

Shopkick rewards you in the form of gift cards (just as good as cash) for actually going into a physical store. All you have to do is link a credit or debit card. So if you actually still need to visit a physical store to buy something last minute you can be rewarded for doing something as simple as scanning a barcode, or your receipt after making a purchase, or by mobile shopping using the Shopkick app.

Note: I recently tried this when I visited WalMart but was unable when I didn’t have a cell or wireless connection inside the store. So hopefully you have better luck in yours!

Drop: Is similar to Shopkick but works more passively in the background. When you first sign up for Drop you are prompted to select 5 brands where you already do a great deal of shopping. The downside I have noticed with Drop is that you are limited to only selecting 5 brands and it does not work for any and all brands where you shop. You also have to link your credit or debit card in order to earn gift cards and cash back for redemption.

Save Money By Selling Your Extra Stuff

We are all familiar with Craigslist. Craigslist has been and continues to be a free marketplace for anyone to buy something they need at a discount from someone else rather than from a store and it allows you to sell anything you don’t need. The average American has 300,000 things (just don’t touch our books) The unfortunate truth is that we are a consumer debt driven society where are default position is to buy and not simplify. There will come a time when debt takes over and a reset button will be forced on us but until that time we are overloaded with stuff. As we have become overloaded with stuff we have become more insular, stressed and anxious.

I am sure you can look around and see some of those 300,000 items as no longer having value and instead turn those items into some green for your pocket, savings and your investing future!

Facebook Marketplace recently came on the scene. It’s obvious advantage is it already has the traffic on the site. CNET goes over 5 primary reasons you should consider using Facebook Marketplace on Craigslist.

TheGoneApp is for anyone looking to buy or sell second-hand electronics. TheGoneApp gives you an instant offer and ships out a shipping box to you.

Gazelle works the same way as TheGoneApp. You input your product details and if you accept the instant offer Gazelle will ship you a box.

Decluttr works just like TheGoneApp and Gazelle but expands into categories such as CDs, DVDs, Games, and Books.

LetGo is very similar to Craigslist with a nice interface.

Offerup is very similar to Craigslist but focuses on your neighbors and community.

Poshmark is for clothes and apparel that you are looking to buy or sell second-hand.

When you want to save money it can seem overwhelming but it doesn't have to be. When you become intentional with your money saving becomes much more natural.

This post will be updated frequently as new saving opportunities emerge. Please let me know if you see any saving opportunities, not on the list below.

Imagine: After days of meeting with private dealers, wiping off the sweat from your brow while leaving dealerships, and test driving what seemed like an endless amount of options, you’ve settled on a car and you’re ready to cut a check and go home. But wait – what about car insurance?

Except after you hand over the check and receive the keys, you can’t drive off yet. You still need to insure your car.

While buying insurance for a car is simple, especially if you already have an insurance provider, it can be a real headache once you see the cost of insurance. Luckily, we've got some tips for you to help save hundreds on your car insurance.

Avoid Overpaying

Always compare prices.

Even if you’ve been with your insurance provider for years, you might be overpaying for your insurance. You can easily save hundreds every year by comparing insurance packages using a service like Gabi, which looks at information from both consumers and car insurers.

Consider Moving

Did you know your geographic location plays heavily into how much you pay for an insurance policy?

Customers living in high-density population states like California, Texas, New York, and others might pay almost $100 more per month on average because of factors like weather conditions, population, crime rates, number of intersections, and insurance requirements by state law.

If you’re already considered moving across state lines, now might be a good time to think about making the switch so you can lower your monthly insurance payments. Even moving from a downtown area into a suburb can lower your policy by a couple of hundred dollars.

Keep a Clean Driving Record

Insurance companies like it when drivers are proactive and avoid costing them money. By avoiding accidents and moving violations, you’ll show your insurance company that you’re a good investment. You can also enroll in a defensive driving course online to help reduce the number of points you have on your license. Your insurance company may provide you with a discount upon completion of the course.

Drive Safely

Another obvious way to lower your policy rates is to avoid reckless driving. there are tons of insurance companies that use in-car devices to help monitor your driving habits. Those habits are tallied up and used to form a “good driver discount.”

One company, Root, has taken this a step further. While many companies require you to already have a policy to qualify for the discount trial, Root allows you to download an app and take a two-week test drive. This will help with your first insurance quote.

Don’t Drive

Another good way to lower your insurance rates is to drive less and utilize public transportation. If you reserve your vehicle for strictly occasional errands and occasional commutes, not only will you save in car maintenance and fuel, but you’ll also be able to lower your premium.

You can also see if your policy providers have a pay-as-you-drive policy which bases your premium on the number of miles you drive. If you don’t drive much, but your spouse or children do, you can save even more money by bundling your policies.

Keep in mind that mileage isn’t a very large factor in car insurance quotes, so shaving off a few hundred miles during your initial quote won’t matter much.

Don’t Drive SUVs or Sports Cars

Though prices may vary by insurance company, sleek sports cars, and bulky SUVs tend to be more expensive to insure than small, unremarkable commuter sedans. The difference in cost is because SUVs and sports cars are often costly to repair, are more likely to be stolen, and are potentially more damaging in an accident.

Because of these same factors, however, some models may have lower premiums, so don’t just avoid SUVs and sports cars entirely. Look for top safety picks and avoid vehicles listed on the National Insurance Crime Bureau’s annual “Hot Wheels” report.

What should you do if you’re unwilling to budget on the car you’ve chosen?

Look for Discounts

Insurers often offer discounts that can be applied to policies, like having lower annual mileage, installing additional safety features, and showing your membership in affiliate groups like AAA. These often aren’t advertised, so you should directly inquire about them.

You should also leverage the length you’ve been driving. Once you reach the age of 20, you’re no longer considered a high-risk driver, and your premium will drop.

This same rule regarding length, however, doesn’t similarly apply to your years with an insurance company. In fact, you might actually be paying more because insurance companies like to engage in price optimization, according to a 2015 NPR report.

Increase your Deductible

In addition to discount seeking, you can go in a bit more of an aggressive and proactive direction by increasing your deductible. Raising your auto deductible means raising the amount of money you’ll pay if you’re in an accident, but, depending on the amount you save on your lowered premium, it may be more beneficial for you financially and create new savings.

Just be sure you have an amount of money equaling your deductible saved in an emergency fund in case you need it!

Saving on Car Insurance

You’ll be surprised just how much money you can save both monthly and annually by trying out these tips. And thanks to the many digital tools, finding and managing these discounts and being proactive in both your car and insurance search is a breeze. Go into your buying process armed with knowledge on how to make the most out of your discounts and you’re sure to come out on top. Learn about the additional ways you can save.

Lexi Carr is a freelance writer with an interest in financial advice, planning, and travel. Please feel free to contact with any inquiries at lexncarr@gmail.com.

There are many financial purchases that can change one's life. And big purchases tend to have the biggest effect. These purchases have their rewards, but they also run therisk of crushing debt and hurting one’s credit score. Bytaking charge of personal finances early, you can decide whether it’s time to take the leap or avoid making the purchase altogether.

College

The first of the big purchases that have exploded in recent years is on college. The amount of people pursuing higher education has ballooned over the past decade. According to theNational Center for Education Statistics, enrollment increased 14 percent between 2005 and 2015. The rise in college attendance has come with a rise in college debt. The average outstanding balance increased 62 percent over the past decade to reach $34,100, according toCNBC. On top of that, about 36 percent of people say they wouldn’t have attended college had they understood the full cost.

College doesn't have to be a mandatory purchase thanks to innovation and technology. To start, there are several places where people can take onlinecollege courses free. Coursera works by providing access to lectures and other material at top schools such as the University of Michigan and Yale University. Udacity provides courses in technology and design, including how to make an iOS app.

Technology jobs are growing rapidly, and many websites are popping up to offer chances to learn coding free. Code Academy is one of the most popular websites, as it has lessons in a variety of coding languages such as HTML and Python. Google alsolaunched a new course that teaches people skills for entry-level IT jobs.

Housing

When it comes to big purchases this is quite often the largest! Other than college, housing is one of the biggest financial purchases in one’s life. The Bureau of Labor Statistics found the average American family spent $18,900 on housing in 2016. Theaverage home value is $217,300 according to Zillow, and that price is only expected to rise in the upcoming year.

Many homeowners end up regretting their purchase. A survey of millennials byBank of the West found 68 percent have some sort of buyer’s remorse, nearly double the number of baby boomers who say they have regrets. Of those with regrets, about one in four says they made poor financial choices when buying their home.

In many cases, renting may be the more practical option.A Trulia study found it’s still 23 percent cheaper for millennials to rent an apartment than buy a home. This is because many millennials can only pay a 10 percent down payment, and there is a chance they may move again after a few years.

Another alternative to buying a house is buying a condominium. Like an apartment, the owner isn’t responsible for exterior maintenance. However, a condo owner can sell their property for a profit in the future. The price depends greatly on the market, so it’s important to buy the condo in the right place at the right time.

Some people are turning to different alternatives, such as buying a “little home.” These homes are expensive to build and have little square footage. But they are easier to tow than a mobile home, they come with standard plumbing and owners pay less for rent at RV parks. Whatever people decide,FinTech helps find the latest technology available for planning a major real estate transaction.

Cars

Transportation is one of the next big expenses in people’s daily lives. TheBureau of Labor Statistics found the average family spent $9,000 on transportation in 2016. Costs include buying a car, yearly maintenance and inspection costs, and the cost of insurance. FinTech Freedomhas tipson the types of insurance people should have, as well as which types people should avoid.

It’s easier than ever to get around without owning a vehicle. Depending on where people live, public transportation is one of the most economical and environmentally friendly choices. Another option is riding a bike or using a public bike-share program. In New York, a MetroCard can cost up to $1,000 a year. Using a Citibike in New York only costs $169 a year.

There are car rental services available for people who need a vehicle on occasions. Zipcar is a car-sharing service with locations around the country. People can rent them at about $10 an hour, or become a member and pay about $70 a year.Rideshares such as Uber or Lyft are another option for daily transportation needs.

And, of course, for situations where owning a car is necessary, consider buying aused vehicle with great gas mileage. While many believe selling a vehicle after purchasing it new is easy, that truth is that new carslose 20 percent of their resale value after being driven off the lot, and 10 percent more over the course of a year. Buying used can save you in the long run, and can often bring you to a car that is just as reliable.

Home appliances

Buying a refrigerator or a new washing machine is a tough pill to swallow after spending money on a new house. Not only are they expensive, but they also run up energy bills.

One alternative to buying a new appliance is buying one that was returned to a major retailer. Another option is buying a used appliance through websites such as Craigslist or NextDoor. There are appliances on those websites that need only minor repairs to run like new again.

Small households can avoid using appliances such as a dishwasher or clothes dryer altogether. Cutting a dishwasher means savings of up to $500 including the initial cost of purchase, and air-drying clothessaves up to $10 a load. Through FinTech, people canfigure out their monthly budget and see which appliances to go without.

Life is full of big money decisions and big purchases, and it's up to consumers to understand all of their options. With the help of FinTech Freedom, making those choices is easier than ever.

Lexi Carr is a freelance writer with an interest in financial advice, planning, and travel. Please feel free to contact with any inquiries at lexncarr@gmail.com.

Maybe lazy is too harsh a term, but who has time to focus on saving?

All too often saving goes out the window because we are busy and it is one more thing on the “to do” list to make a conscious effort. The reality is that most full-time workers live paycheck to paycheck.

Save time and money with a little help from 5 of your newest friends:

Paribus

Paribus puts money back in your hands on the online purchases you are already making with no effort from you. You’re probably thinking – no way. How does that work?

Paribus makes it easy. It is free to sign up and it gets right to work scanning your emails for receipts. If it discovers you made a purchase from one of the retailers listed on their website, it will track the item’s price. If the price drops, Paribus requests a refund for you – automatically!

See? You really don’t have to do anything.

Dosh

Dosh is the definition of hassle-free cash back. Sign up for the app and tie it to a debit or credit card (did we mention you get a $5 bonus just to sign up?)

Make purchases with this card at over 100,000 hotels, online stores, and restaurants. Watch as your cash back rolls in.

Shopkick

Download the Shopkick app and go shopping! Once you sign up the app pays you for “kicks” for walking into participating stores (Amazon, Walmart, TJMaxx and many more.)

Your kicks count increases for scanning items in the store and purchasing them with a connected credit or debit card.These kicks can be redeemed for store gift cards.

Trim

Don’t lose time negotiating monthly bills with service providers, let Trim do that for you.

Sign up with Facebook and upload a PDF of your recent bill. Trim gets to work negotiating your rates for you and it will continue until you save money. Trim works with Time Warner, Comcast, and other major providers.

Phil

Do you love going to the pharmacy? I can imagine that you are with the 50% of Americans who take prescriptions and share the “joy” of standing in line at the pharmacy.

Stop wasting time in line with Phil – the online prescription delivery system. Phil coordinates with pharmacies, doctors and insurance providers to fill your scripts and ship them to you to the tune of your usual copays – delivery is free.

Download. Attach. Save. It is really that simple – so get saving!

Saving Can Be Easy.

Saving for your future has never been easier thanks to the increasing number of innovative online fintech companies.