US 10-Year Treasury Yield…

July 1980: 10.1%

July 1985: 10.5%

July 1990: 8.5%

July 1995: 6.5%

July 2000: 6.0%

July 2005: 4.3%

July 2010: 3.0%

July 2015: 2.3%

July 2020: 0.6%

— Charlie Bilello (@charliebilello) July 23, 2020

Learn about the latest investing startups in fintech. Investing is the foundation for setting you up for the future. It is impossible for most people to ever be able to earn their way to a prosperous retirement. Historically, investing was only available to a select few. Today, it is open and available to everyone and at a cost that most can afford. Here you will find the latest tools and technology available to you for investment as well as an explanation of these new investing options. Here is an example: 4 Easy Ways To Focus On Your Retirement Investing.

US 10-Year Treasury Yield…

July 1980: 10.1%

July 1985: 10.5%

July 1990: 8.5%

July 1995: 6.5%

July 2000: 6.0%

July 2005: 4.3%

July 2010: 3.0%

July 2015: 2.3%

July 2020: 0.6%

— Charlie Bilello (@charliebilello) July 23, 2020

Charlie Bilello over at Compound Advisors just recently published this great article…“Put These Charts On Your Wall…2020 Edition“

I am a big fan of Barstool Sports. Dave Portnoy is hysterical in this clip on CNBC.

This article discusses passive income investing options. FinTech Freedom is not responsible for investing loses or risks. Please see our disclosure statement.

Just the term “Passive Income” brings with it feelings of joy and excitement! Passive income generally involves either an investment in time or money. This post will highlight ways to generate passive income using money not time. Passive income where time is involved generally includes a side hustle often classified within the various opportunities found within the gig economy.

One of my favorite stories on investing money comes from Tim Ferris. Tim tells the story of how he created his own real-world MBA. In short, instead of going to Stanford business school to get his MBA he took what he would have spent on the MBA ($120,000) and invested it as an angel investor in $10-$50,000 increments.

Two important things to keep in mind. The first is to make sure that you only invest and put money into what you understand. Secondly, it often helps to invest in what interests you.

Among the various passive income ideas, these are the most popular and appear most frequently.

Build a Monthly Passive Dividend Paycheck with Dividend Stocks – WalletHacks

Owning equities such as stocks and bonds is one of the easiest and most efficient ways to generate passive income. This strategy requires the discipline to save and invest. We recommend using an index fund in the form of either a mutual fund or exchange-traded fund (ETF). Using an index fund allows you to get diversification at a very low cost as well as the simplicity of a couple of funds instead of a number of stocks. An S&P 500 index fund, as well as a broad-based bond fund composed of government, corporate and municipal bonds in addition to an Index real estate investment trust (REIT), represent three great areas to start which brings broad diversification.

How I Earn Over 10% Passive Income With P2P Lending – Financial Samurai

Prior to the exponential growth of the internet, it was impossible for anyone looking for a loan to receive a loan unless they had access to or a relationship with a bank. Thankfully, this is no longer the case! Today, online peer to peer lending allows almost anyone access to a loan. Not only does this allow for greater access but it is also cheaper for borrowers given the greater level of competition with banks as well as other online outlets. On the flip side – online borrowing with peer to peer loans gives investors the opportunity to passively earn a return on their investment. Borrowers involved in peer to peer lending can experience a lower interest rate than they would from a bank while investors experience a greater return on their money than if that money were to sit in a bank account. The result? A win-win with higher earning potential for lenders and lower borrowing costs for borrowers.

An important note, with the current record level of consumer debt you may want to tread lightly here. Or – at the very least – make sure that your investments are well diversified from risky to less risky. Two of the largest peer to peer lending platforms are Lending Club and Prosper. Nerdwallet has a great comparison chart outlining the pros and cons of both platforms.

As an example to show the opportunity for both borrower and lender, say the borrower wants to borrow $5,000 to remodel their kitchen. Peer to peer lending allows the borrower to get a loan for 6% vs. 8% from the bank. The lender gets a return of 4% vs. 2% for keeping their money in a bank. Before peer to peer lending the bank would be able to keep a profit of 6% (8% minus 2%) Peer to peer lending enables the borrower to save 2% and the lender gets a 2% larger return on their money. Consequently, both borrower and lender come out in a better position with peer to peer lending than if they would have used a traditional middleman (bank)!

Small business investing and lending can be lucrative and act as another creative way to diversify your investments. It also carries risk just as any other investment does. In most cases, you are lending to help fulfill inventory requirements against a purchase order. Platforms in this space include Funding Circle, KickFurther, Street Shares, and Kabbage.

Real Estate Crowdfunding – Financial Samurai

Real estate crowdfunding is a relatively new entry to the passive income market! Real estate crowdfunding investors can invest small amounts of money in real estate property anywhere without the hassle of having to deal with the headaches that come along with being a landlord. There are now dozens of online platforms that allow you to become a direct investor in specific real estate projects. Two of the most comprehensive crowdfunding comparison resources I have found online is over at investorjunkie.com and FitSmallBusiness.

Another way to gain exposure to real estate and earn passive income is with a REIT.

13 Ways to Make Extra Cash Renting Out Your Stuff – Part-Time Money

20 Things You Can Rent Out For Extra Money – Vital Dollar

Today, you can rent out almost anything that you own. Large ticket items such as real estate and vehicles can be rented out on places such as Airbnb and Turo. Beyond large ticket items, it is now possible to rent out almost anything you may have just lying around!

When Ms. Cafe Career Coach and I begin to build our dream home we can’t wait to slap on the amazing Tesla Solar Roof! Until then, one way to earn money from solar is to invest in it! With Wunder Capital, you can do just that!

An additional possible passive income source that is worth checking out is to try and find missing money using either Unclaimed.org and MissingMoney.com.

One popular way to make money somewhat passively is online. We wanted to include a couple of articles on how best to make money online even though these ideas primarily fall into the category of a time commitment side hustle. Over time it is possible for the time commitment required to evolve into a significant passive income which is why we decided to include the following articles to get you started.

How To Make Money Online: 34 Ways You Can Start Earning Today

17 Ways To Earn Extra Money Online This Month

How to Make Money Online: 21 Ways to Make Money From Your Laptop

Other great articles on passive income can be found over at: MoneyPeach, Club Thrifty, Vital Dollar, Well Kept Wallet, Millennial Money, Making Momentum and a personal favorite from Financial Samurai.

With companies like Wrapify, Carvertise, and Free Car Media you can have a company pay you to place an ad on your car.

Never before has it been this easy to achieve passive income to invest and earn money online. Thanks to new fintech companies that are springing up there are many to choose from!

The Following Post Is a Guest Post from ClubThrifty

Google “make more money” and you’ll come up with about 4.5 billion results! Seems like quite a few of us are trying to improve our financial situation, huh?

When it comes to increasing income, we’ve all heard catchphrases like “in less than 30 days” and “in your spare time”. While many work-from-home options are totally legit, the majority won’t net you any significant increase in income.

If your goal is just an extra $20 here and there for fun, that’s fine. Sure, you can make a few bucks taking online surveys. Absolutely, you can take on a new part-time job. There’s nothing wrong with those methods.

What we’d like to focus on right now, however, is good, straightforward methods you can use to build significant wealth, without the gimmicks. So, if your primary goal is to increase your income in a life-changing way, you’ll want to keep reading! We’ve got some of the best strategies for you to start building real wealth.

Eventually, we all have to leave our working days behind, and planning ahead for that is crucial. If you don’t want to be stuck eating rice and beans in retirement, you need to zero in on your retirement plans.

A popular way to save for retirement is by utilizing a retirement account like a 401(k) plan. As an employer-sponsored retirement account, the 401(k) enables workers to invest a portion of their income automatically every month.

Earnings in a traditional 401(k) are tax-deferred, so your contributions – as well as the earnings from them – are only taxed when you withdraw those funds at retirement age. For many, this is especially appealing because you get to keep more of your money up-front.

Investing in a 401(k), 403(b), or similar work-sponsored account can also help you build wealth through a company match. For example, your employer may match up to 4% of what you put in. These “free money” contributions can be an excellent way for you to save even more toward your retirement goals.

Take advantage of the power of time and compound interest. The sooner you can start and/or increase your contributions in a 401(k), the more time you give your money to grow!

Real estate is one of our favorite ways to diversify our income streams and build more wealth.

While retirement accounts are important for your future, real estate differs in that it offers you substantial income in the present. In addition to (hopefully) increasing in value, the rental income from your property can provide a nice bump in monthly income, as well. Then, down the road when you decide to sell, you’ll also receive the profits from the sale.

If owning real estate appeals to you but you’re turned off by some of the downsides (like expensive down payments and the hassle of maintenance issues), take some time to review companies like Fundrise. They’re essentially crowdfunded real estate opportunities that enable investors to get in on the action for as little as $500.

Whether you’re more interested in a brick-and-mortar property or a crowdfunding option, real estate provides some amazing opportunities to really gain momentum in your investments.

Starting a business is a powerful wealth-building tool because there’s no ceiling on potential income! Going into business for yourself can sound really intimidating. I get that. But the perks of being an entrepreneur are many.

Although it isn’t always possible, an ideal business is one that enables you to earn passive income. That way, once the business is set up, you can begin increasing your profits without investing too much more time or effort. If you can find yourself a good personal gig that earns significant passive income, that’s a pretty sweet way to build your wealth.

For example, when you write a book or create an educational course, you put a ton of work into it. Once it’s done, however, you can continue earning money off its sales for years to come!

We’re pretty passionate about this one. If you’re trying to build real wealth, consumer debt acts like a giant weight hanging around your neck. While getting debt-free might be less exciting than earning extra money, it’s a crucial step on the path to building true wealth.

Although many Americans consider debt to be a “normal” fact of life, that doesn’t mean you have to! Think about it: Do you want to continue sending half your paycheck to somebody else every month, or would you rather keep that money for yourself?

The answer is pretty obvious, right? Honestly, just imagine the possibilities if you weren’t stuck up to your neck in consumer debt. They’re practically endless!

Credit cards, car loans, student loans – they’re like a trap. As you know, most loans come with hefty interest charges, so you end up paying a lot more for everything than it originally cost.

Debt also destroys your ability to save and build wealth. That’s why it’s imperative to get yourself out of debt as soon as humanly possible. I mean, get yourself laser-focused until it’s gone!

The average monthly car loan is now over $500! If you’re paying on two cars, that could be $1,000 a month just in car payments! That’s insane!!!!

What could you do with an additional $500, $600, or even $1,000 a month? Maybe you could save for a down payment on a house or invest that money and retire early. Perhaps you could take a chance on a new career. Or, maybe you could just enjoy the freedom of no longer living paycheck to paycheck.

Whatever your big goals are, you’ll get there much faster once you destroy your debt!

Let’s face it – we’re all sick of money-making gimmicks…but that doesn’t mean there aren’t legitimate ways to grow your wealth! You can make some serious bank and increase your net worth with any one of these strategies we’ve talked about.

Destroy your debt, save for retirement, invest in real estate, and maybe even start your own business. Use a few of these ideas together, and you’re looking at some real, significant wealth-building potential! At the very least, you’ll be on the path to retirement, leaving a positive legacy of sound money management for your loved ones to learn from in the future.

For additional investing and wealth building articles please see our investing category.

Kate Underwood is a freelance writer and staff writer for Club Thrifty, a website dedicated to helping people dream big, spend less, and travel more.

How are you saving for real wealth? Let us know in the comments!

Investing can be overwhelming and confusing. The truth is that it is neither and this article will show you just how simple investing can be…

“Money can buy many things, but nothing more valuable than your freedom…Stop thinking about what your money can buy. Start thinking about what your money can earn.” – “The Simple Path to Wealth: Your roadmap to financial independence and a rich, free life” by JL Collins

I just finished reading The Simple Path to Wealth by JL Collins after it was recommended by a number of other bloggers such as Mr. Money Mustache, Four Pillar Freedom, The Power of Thrift, and J. Money over at Budgets Are Sexy.

JL Collins (who also just happens to live in New Hampshire!) was first published in 2016 but is one of those books I wish had been published years ago. The Simple Path to Wealth outlines not only a clear outline for investing but also a thorough rationale for this simple approach.

JL has a number of hard-hitting and poignant lines from his book – some of which I will include below for more context. Quite frankly, he gets to the point much clearer and succinctly in the passages below and his book than I ever could!

The first step to investing and growing your wealth is to avoid debt at all costs! Here’s the simple formula: Spend less than you earn—invest the surplus—avoid debt”

Now, some may take issue on this point considering the fact that many people have debt in the form of a mortgage. I am not suggesting that you hold off investing in the stock market until you have your mortgage paid off. Instead, here is where I suggest following the 7 Baby Steps by Dave Ramsey.

In the spirit of the book, I will also keep this analysis of the book simple and straightforward. In short, JL Collins advocates investing in one simple broad-based index fund from Vanguard known as VTSAX. VTSAX is the Vanguard Total Stock Market Index Fund Admiral Shares. JL writes…“Put all your eggs in one basket and forget about it. The great irony of investing is that the more you watch and fiddle with your holdings the less well you are likely to do.”

It is worth noting that there are a couple of comparable exchange-traded funds that will perform almost exactly the same way. Here are some of the most common: VTI, ITOT, SCHB. Depending on where you do you investing each one might make more sense than the other. For example, VTI is a Vanguard Fund, ITOT is a iShares Fund (Ideal for Fidelity customers) and SCHB is a Charles Schwab Fund. So, if for example, you are a Fidelity customer you should probably go with ITOT because it is $0 to trade. One important thing to note is that just because you are a Fidelity customer (using this example) you are still able to purchase VTI and SCHB but Fidelity charges a one-time trading fee which also holds true for both Schwab and Vanguard.

Another option in place of a fund like VTSAX or ETFs like VTI, ITOT, and SCHB is to invest in the S&P 500. The S&P 500 makes up approximately 80% of the broad-based funds mentioned above. You can't go wrong either way. It may be worth going with an S&P 500 fund.

Why One Simple Fund?

It’s fairly simple. Here is JL in his own words…

I wanted to simplify

I wanted to be lazier

I wanted extremely low fees

I wanted to own everything and be completely diversified all at the same time

Said another way:

“Simple is good”

‘Simple is easier”

“Simple is more profitable”

“Avoid the trap of complexity”

An important statistic to keep in mind for those that embrace this one simple approach is that it will outperform 82% of actively engaged investors.

JL points out three important reasons to ignore going into additional international funds.

In short, no! Thanks to technology it has never been easier or cheaper to invest in low cost broadly diversified index funds and exchange-traded funds. JL Writes…

“Be wary of anyone who makes their living making money managing your money. There is far more money in recommending complex investments, not simple low-cost ones. Advisors are not drawn to the best investments but those that give them the largest commission. You not only lose the money by giving a commission but the future opportunity that money could have compounded to work for you. Avoid annuities and whole life insurance. Advisors are only as good as the investments they recommend. Since those are mostly actively managed funds as opposed to the passive low-cost index funds how often do those outperform? Very rarely! About 20% outperform in any given year and looking at a 30 year period that drops to less than 1%. So, you can learn to pick your advisor or learn to pick your investments. The latter is cheaper and will prove to be more beneficial. No one will care more about your money more than you.”

Dollar cost averaging is just a fancy way of investing over a period of time in small increments. It’s important to note that if you invest in a 401K or any other pre-tax retirement account each time you are paid you are using dollar cost averaging. The Simple Path To Wealth points out that statistically, the market goes up 77% of the time. Therefore, by engaging in dollar cost averaging outside of traditional individual retirement account investing where you have no other choice but to wait until you have the money and or are paid for your work you would be actively engaging in market timing which is a loser's game.

It can be easy to forget just how lucky we are for even having the opportunity to read this article on a computer, phone or tablet online. One of the sites that is mentioned in The Simple Path To Wealth can be found at the Global Rich List. I recommend taking a few minutes to visit this site by inputting your individual income and wealth levels. You might be surprised to see where you fall!

If you are interested in reading more I encourage you to visit JL Collins website. In particular, the stock series. Another helpful article is “Outperform 99% of Your Neighbors”

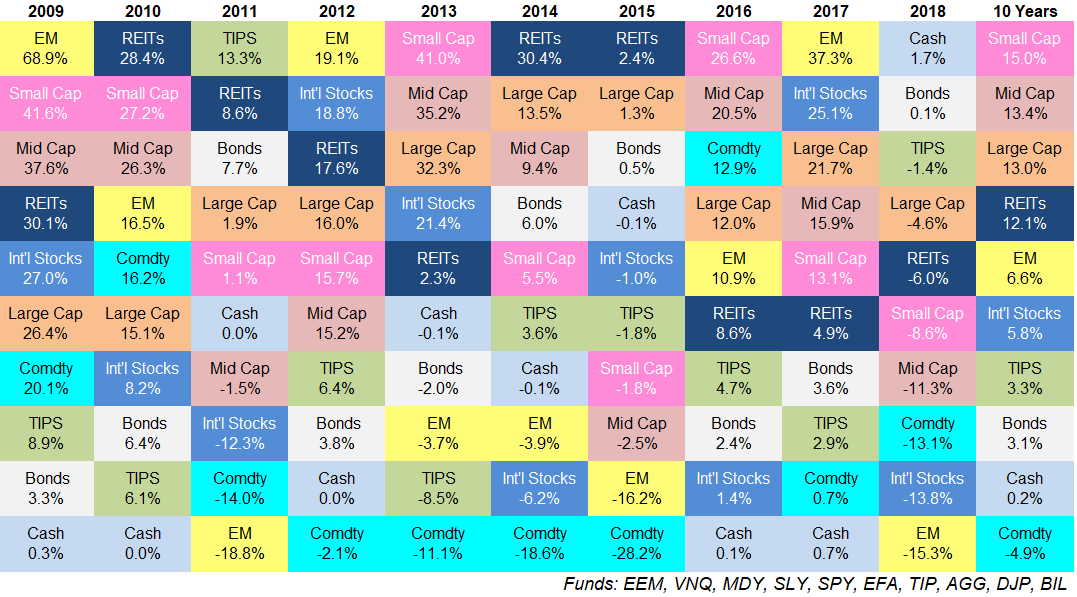

A reminder about the importance of diversification. This chart shows how the different major asset classes can yield a new and different return on investment each year. Once again, as the saying goes…the only free lunch when it comes to investing is diversification.

As someone who is just starting out blogging, I think it is important to highlight the personal finance bloggers that I look forward to reading as soon as they post new content!

In no particular order here are my favorite personal finance bloggers…

Sam over at Financial Samurai is a great writer who writes primarily about investing and wealth building. Sam is able to make the highly complex simple for the average reader interested in how best to build long-term wealth. Hint: Make sure you sign up for his email newsletter. There are topics and articles that he writes about that don’t get placed on the website.

Ben Carlson over at A Wealth Of Common Sense is similar to Sam in that his writing style makes it easy to understand what quite often aren’t fundamental personal finance topics. As good as the content on the blog is I would say his weekly Animal Spirits Podcast that he hosts with Michael Batnick is even better!

Andrew and Tom host the Listen Money Matters Podcast together where you can not only learn about some new beers you can try out but also various topics pertaining to personal finance. The content layout and design of Listen Money Matters is well worth a look!

Mike Piper over at Oblivious Investor was the first personal finance blogger I discovered. Mike’s Made Simple series of books is a wonderful series showcasing the most important topics of personal finance in a digestible format that readers can easily understand.

Grant over at Millennial Money has done an amazing job putting together a number of resources for his readers. His Podcast covers a new topic in 5 minutes or less! Remember…simplicity is essential!

The Penny Hoarder is an absolute machine when it comes to putting out new content. They have a wealth of content that covers a number of personal finance topics. The content is generally short and easy to quickly read.

Pete is Mr. Money Mustache and came onto the scene with his first post all the way back on April 6, 2011. Mr. Money Mustache writes incredibly well and has an in-depth style in his writing for readers looking for lengthy writing descriptions. For example, one of my favorite posts is “The Practical Benefits of Outrageous Optimism” is one of those posts that really makes you think and I find it especially beneficial for those with a high analytical way of thinking.

Zach over at Four Pillar Freedom does a great job putting out new great content on a consistent basis! While you are there check out his brand new monthly spending app!

If I get to meet all of these bloggers at FinCon18 in Orlando in September I would be thrilled! If not, at least I know I will get the chance to meet a number of other great bloggers from the Rockstar Finance community!

Who are your favorite personal finance bloggers? Leave a comment below or feel free to contact me with any others I should have mentioned here!

I recently came across the 2014 Fidelity study which showed that the people who were the best investors were the ones that completely forgot that they had an account. Knowing this – we can be our own worst enemies when it comes to investing for the future. It is human instinct to believe that we can invest in a better way or are smarter than everyone else…

Here is the bitter truth…it is impossible to know what the stock market will do in the next minute, the next hour, the next day or the next week! In fact, pick any future time period. It is impossible!

So why would you invest in anything on the stock market that is anything other than the 500 largest companies in the United States? In fact, just by owning these 500 largest companies in the United States you would also – by extension – have exposure to the rest of the World given the fact that the majority of these companies do a significant amount of business overseas.

So, why bother with an expensive money manager, financial advisor, and the expensive products that come with them? It’s because despite you now knowing it’s impossible to predict the future you still believe that you can…

So say it 3 times out loud…I can’t beat the market…I can’t beat the market…I can’t beat the market!

Why The S&P 500?

In the great book by Burton Malkiel “A Random Walk Down Wall Street” he writes, “Stock investors can do no better than simply buying and holding an index fund that owns a portfolio consisting of all the stocks in the market.” The S&P 500 represents the 500 largest and most profitable companies in the U.S. These 500 companies make up anywhere between 78% – 80% of the total U.S. stock market. There are certainly other viable potential portfolios you can select but there is something to be said for simplicity.

As someone who believes in the power of technology and the impact that fintech startups can have on personal finance, it can be easy to make things complicated. Instead, I try to always make sure that whatever effort I am putting forward in new technology that serves a specific purpose. The S&P 500 is as simple, straightforward and as easy as it gets!

If you watch the following great talk by JLCollins at Google and fast forward to the 45:50 mark you will see just why the S&P500 is a great option. By the way, VTSAX which JLCollins also recommends and invests in is also a good solution for certain investors.

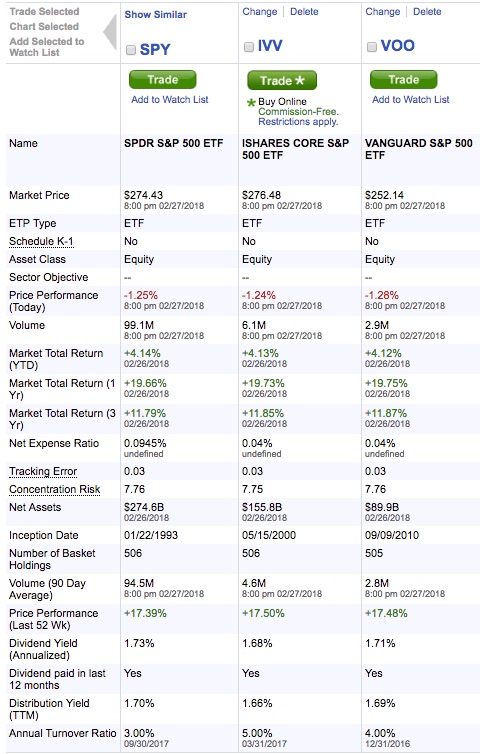

The 3 top ETFs according to Investopedia are SPY, IVV, and VOO. I took a screenshot of these 3 using the Fidelity compare tool where I am an investor. IVV is offered free to trade and is tied for the lowest expense ratio at 0.04% with VOO. So for me…IVV was the choice! It's important to note that VOO is commission free if you are a Vanguard customer buying it through Vanguard's website. The chart below is a Fidelity chart. Therefore, it only shows IVV as commission free. Thank you to sa_node on Reddit for pointing out this important distinction and fact. Investing does not need to be complicated!

The blog Monevator recently shared the following video which helps to clarify the point of this article.

Please note: FinTechFreedom is a financial publisher that does not offer any personal financial advice, or advocate the purchase or sale of any security or investment for any specific individual. Members should be aware that investment markets have inherent risks, and past performance does not assure future results. In accordance with FTC guidelines, FinTechFreedom has financial relationships with some of the services mentioned and may be compensated if consumers choose to click these links and ultimately sign up for them. To read more please visit the Disclosure Statement.